Windows App

Windows App  MacOS (sillicon)

MacOS (sillicon) How Barie drafts a regulatory compliance checklist for a fintech launching a lending product in the UK

Barie researches FCA requirements, licensing obligations, and recent enforcement actions from live regulatory sources. It delivers a jurisdiction-specific, current-as-of-today compliance checklist — every requirement linked to its regulatory origin. Not a generic template pulled from a law firm blog that may not reflect current FCA guidance.

The problem with chat-based compliance guidance

A fintech founder asked an AI tool for a compliance checklist before launching a UK lending product. The output was four pages long. It covered consumer credit authorisation, affordability assessments, financial promotions, and CASS. It looked thorough.

It was missing the FCA’s Consumer Duty — the most significant new requirement in UK financial regulation in a generation, effective from July 2023. Any lending product launched without Consumer Duty compliance embedded in the product design, customer journey, and board governance was launching into enforcement risk from day one. The checklist did not mention it once.

Regulatory requirements are not stable. The FCA publishes new guidance, Dear CEO letters, and supervisory expectations on a rolling basis. A checklist drawn from training data reflects what compliance looked like when the model was trained — not what the FCA currently expects.

Why UK lending compliance specifically requires live sources: The FCA’s Consumer Duty (PS22/9, effective July 2023) fundamentally changed the obligation framework for retail lending. The FCA’s Consumer Credit sourcebook (CONC) is updated regularly. Recent enforcement actions reveal current supervisory priorities that do not appear in the published rulebook. Any compliance checklist that does not incorporate all three is incomplete.

Your prompt

Task prompt

“Draft a regulatory compliance checklist for a fintech launching a lending product in the UK.”

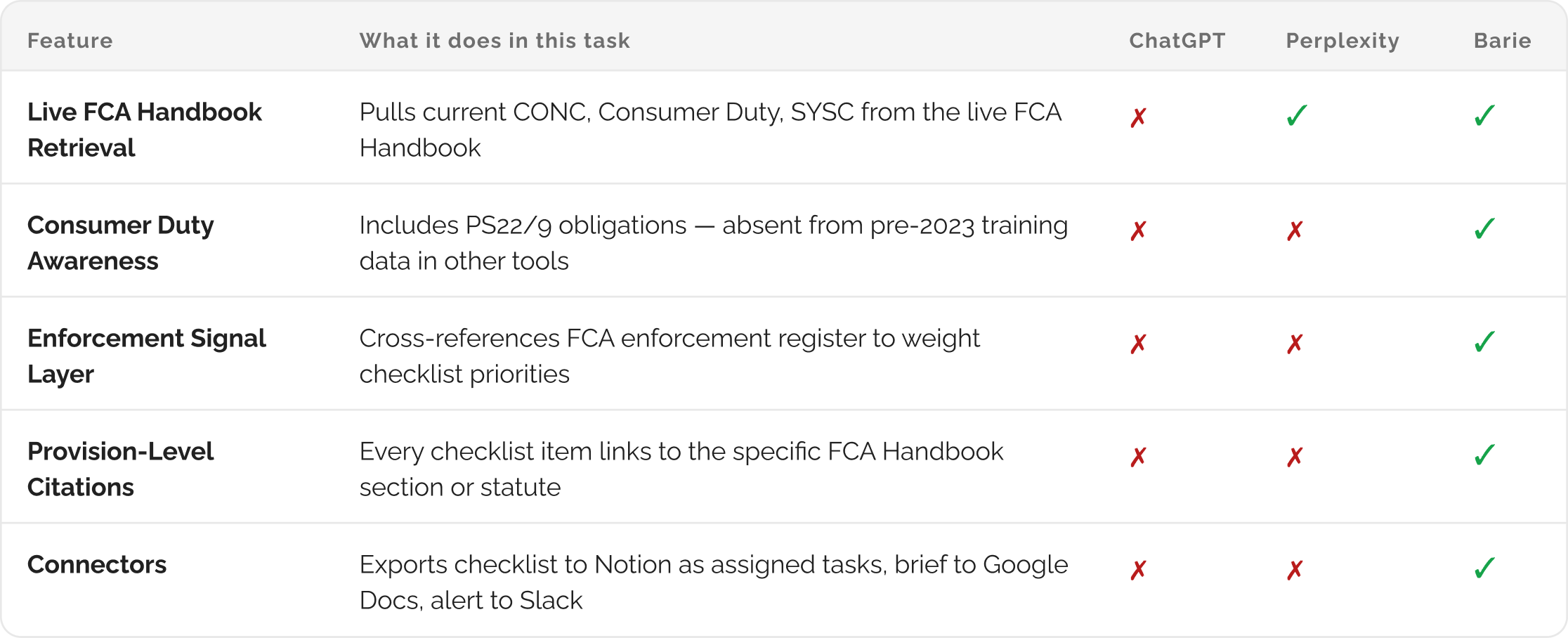

One sentence. Barie identifies the relevant regulatory frameworks — FCA Consumer Credit authorisation, CONC, Consumer Duty, CASS, UK GDPR, AML/KYC, and financial promotions — retrieves the current requirements from live FCA sources, cross-references recent enforcement actions for supervisory signals, and assembles a prioritised checklist with each item linked to its regulatory origin.

1: Task Decomposition

Step 1: Task decomposition — frameworks, sources, and priority tiers

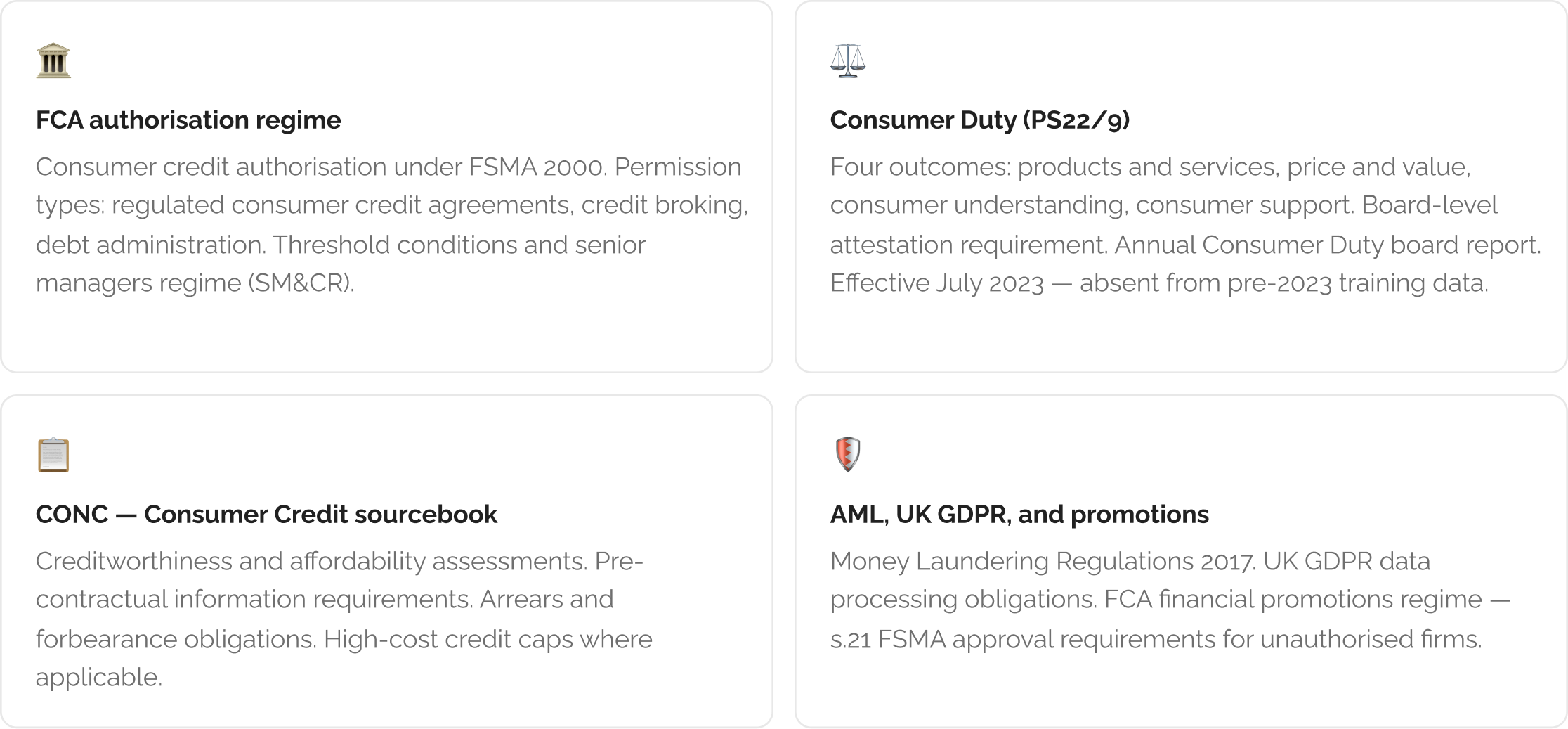

Before retrieving a single requirement, Barie maps the regulatory landscape for UK consumer lending. This is not a single-framework question. A fintech launching a lending product in the UK faces obligations across at least six distinct regulatory frameworks simultaneously.

Priority tiers assigned before retrieval: Barie classifies each requirement into three tiers — Must (pre-launch hard blockers, enforcement risk if absent), High (required but with lead time), and Best Practice (supervisory expectation without explicit rule). The checklist reflects this tiering so a founder knows what to resolve before day one versus what to build toward.

2. Live Regulatory Research

Step 2: Live retrieval — FCA Handbook, enforcement register, and recent guidance

Barie retrieves requirements from three source types simultaneously: the current FCA Handbook for the operative rule text; recent FCA Dear CEO letters and supervisory statements for current enforcement priorities; and the FCA’s published enforcement case register for signals about what is actively being actioned.

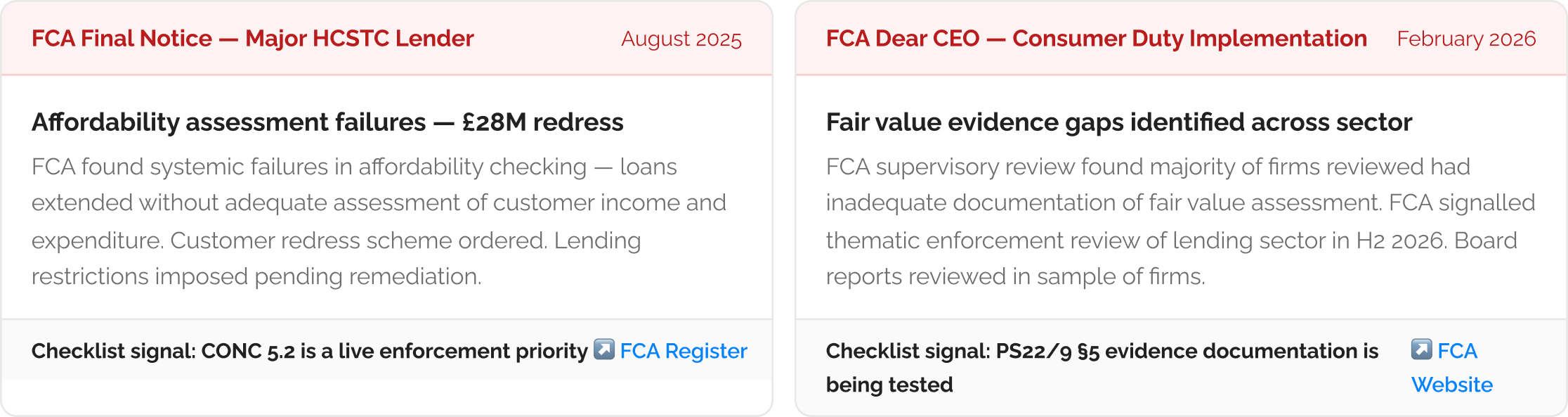

The enforcement register is what most checklists miss: The FCA’s published enforcement cases reveal where supervisory attention is currently concentrated — and where requirements that appear technical in the rulebook are being treated as material in practice. Barie retrieves recent lending-related enforcement decisions and uses them to weight the checklist priority tier. A requirement that appears in three enforcement cases in the last 12 months is treated as a must-fix, not a best-practice note.

3. Compliance Checklist Output

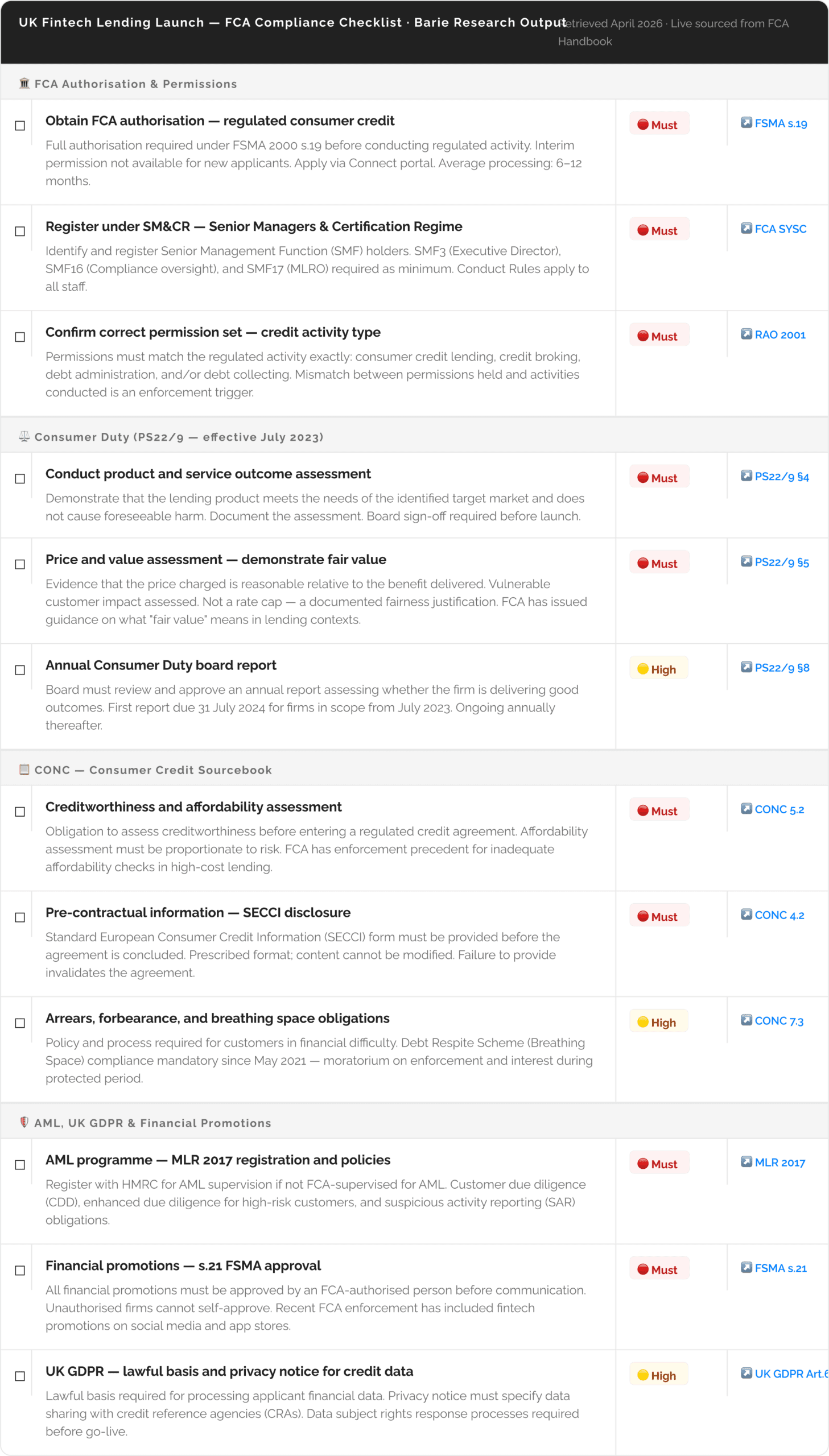

Step 3: The compliance checklist — every item sourced, prioritised, and current

Every item links to its regulatory origin: The source column in each checklist row links directly to the FCA Handbook section, Policy Statement, or statutory provision that generates the requirement. The checklist is not asserted — it is grounded. If the FCA updates a requirement, the source link takes you to the current version of the rule, not a cached copy.

4. Enforcement Signal Layer

Step 4: Enforcement signals — what the FCA is actively actioning right now

The published rulebook tells you what is required. Recent enforcement cases tell you where the FCA is currently looking. Barie retrieves both and surfaces the enforcement signals that should weight your prioritisation — requirements that appear routine in the Handbook but are generating active enforcement in the lending sector.

5. Export via Connectors

Step 5: Export — checklist to Notion, brief to Google Docs, alert to Slack

![]()

The full checklist lands in Notion as an interactive document — each item is a checkable task with its source link embedded, assigned to the relevant team owner (legal, product, engineering, compliance). A formatted version exports to Google Docs for external counsel review. A summary of the Must-tier items goes to Slack before the pre-launch review meeting.

The Notion checklist is a living document: Because every requirement links to the current FCA Handbook URL, the checklist remains accurate as the Handbook is updated. When the FCA revises CONC or issues new Consumer Duty guidance, the source link reflects the current requirement. The checklist does not become outdated — it becomes a reference point you verify at source whenever the regulatory environment shifts.

What you get

A jurisdiction-specific, current-as-of-today compliance checklist for a UK fintech lending launch — covering FCA authorisation, Consumer Duty, CONC, AML, UK GDPR, and financial promotions. Every requirement sourced to the FCA Handbook section or statutory provision it comes from. Priority-tiered into must-fix pre-launch items and build-toward requirements. Enforcement signals from recent FCA cases layered in to weight the prioritisation.

What it would take a compliance consultant a day to assemble — mapping six frameworks, retrieving current requirements, cross-referencing enforcement, formatting a checklist — Barie delivers in one prompt. Current. Sourced. Ready to assign.

The Verdict

A compliance checklist that misses Consumer Duty is not a checklist. It is a liability. The FCA’s most significant new obligation for retail lending — effective since July 2023, actively being tested in supervisory reviews in 2026 — is absent from any checklist built on pre-2023 training data. Barie retrieves from the current FCA Handbook, surfaces the enforcement signals from recent cases, and delivers a checklist where every requirement is current, every item is sourced, and nothing material is missing because the model’s training data predates the regulation. That is the difference between a compliance tool and a liability.

Barie features used in this task